Understanding the L Funds

The L Funds are designed to provide a diversified portfolio that automatically adjusts over time.

Each fund follows a predefined glide path, gradually shifting from a higher allocation to equities toward a more conservative mix as the target date approaches. The goal is to simplify long-term investing by aligning the portfolio with a general retirement timeline.

This structure allows participants to maintain a diversified allocation without needing to make frequent adjustments

A set framework, not a tailored solution

Because the L Funds follow a standardized structure, they are intentionally limited in what they can take into account.

L Funds do not incorporate individualized information such as:

• Assets held outside the TSP

• Pensions or other income sources

• Career changes, pay variability, or contribution timing

• How savings are split between Traditional and Roth accounts

• Personal tolerance for volatility or drawdowns

This is not a flaw, it is a constraint. Defaults are designed to work reasonably well for many participants by relying on a small set of stable assumptions. That same simplicity, however, means L Funds cannot adapt to individual decisions or circumstances, and coordination across a household’s broader financial picture.

Understanding this distinction helps clarify what L Funds are designed to do, and where their role naturally ends.

What you’re deciding by default

Choosing, or staying in, an L Fund by default is not a neutral choice. It embeds assumptions about:

• When you will retire

• How much income you’ll need

• How much risk you can absorb

• Your TSP withdrawal strategy

• How other income sources (pension, Social Security, investments outside your TSP) will support you

The L Fund makes these assumptions for you, and then follows them consistently, regardless of how your career, income, or priorities evolve. For some participants, those assumptions remain reasonable. For others, they quietly drift out of alignment over time.

Investment timelines

The L Funds are built around a specific timeline, but that timeline does not mean the portfolio ever becomes static.

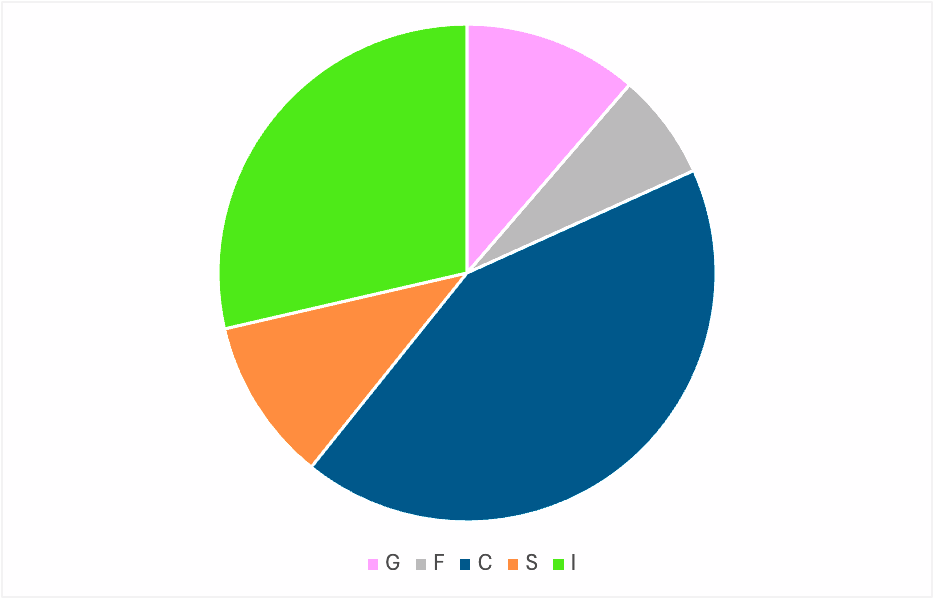

Even the most conservative L Funds continue to hold exposure to all five core TSP funds. This includes stocks, even in retirement-focused allocations.

This is intentional.

Retirement is not a single point in time. It is a multi-decade period during which the portfolio still needs to support growth, income, and inflation over time.

Because of this, L Funds are designed to balance stability with continued exposure to market growth, rather than shifting entirely into fixed income.

The result is a portfolio that gradually becomes more conservative, but still maintains diversification across asset classes throughout the full investment horizon.

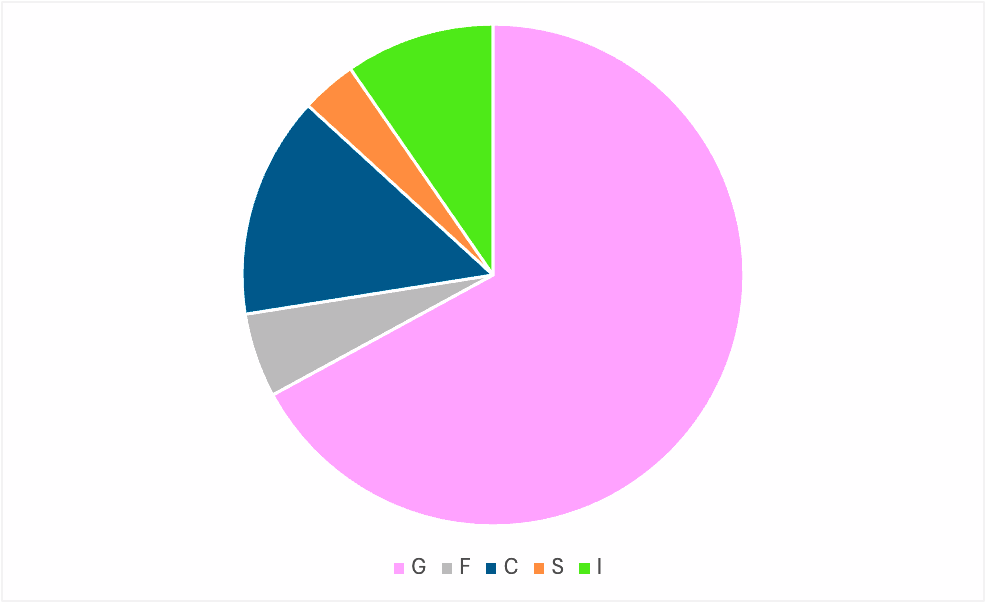

L 2075

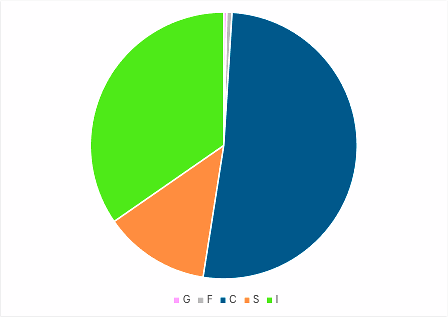

L 2050